A Crisis of Confidence

Have you ever reflected on the foundation of the financial system? What comes to mind? Banks, investors, the stock market, the bond market, or the credit markets? That’s partially true. They are the underpinnings, but the foundation or the bedrock of the financial system is confidence. Without confidence, we are left in a very precarious situation.

We have full confidence that when we withdraw cash from a bank account or money market fund, or for that matter, close out an account, we will have immediate access to those funds. But bank vaults aren’t filled with cash that can be easily repatriated to depositors if, by an incredible long shot, everyone shows up one day to close their account. Our deposits are invested in high-quality bonds, Treasury bills, and loans.

We have full confidence that when we withdraw cash from a bank account or money market fund, or for that matter, close out an account, we will have immediate access to those funds. But bank vaults aren’t filled with cash that can be easily repatriated to depositors if, by an incredible long shot, everyone shows up one day to close their account. Our deposits are invested in high-quality bonds, Treasury bills, and loans.

What happened at Silicon Valley Bank last month was simply an old-fashioned bank run. Why? Confidence quickly evaporated. But the root cause of its demise had many regulators, investors, and Fed officials scratching their heads because nearly everyone was caught off guard.

A far cry from 2008

Unlike 2008, when major banks were saddled with bad real estate loans, SVB invested heavily in a portfolio of high-quality, longer-term Treasury bonds. From a credit standpoint, these are super-safe investments. What could go wrong? Well, nothing if the bonds were held to maturity or if interest rates had remained stable.

Bond prices and bond yields move in the opposite direction. When yields rose, the bonds fell in value, creating a paper loss. But its customer base of venture capital investors had been drawing down on their deposits as more traditional sources of funding were drying up. With deposits being drawn down, SVB was forced to sell $21 billion in bonds, and the bank took a nearly $2.0 billion loss. SVB’s hastily announced plan to raise capital was quickly scuttled when its stock tumbled, and depositors quickly began to withdraw cash, since a large majority of the bank’s deposits were above the FDIC limit.

Less than two days after the bank revealed its loss on the sale of Treasuries, regulators were forced to shut the bank. Time to failure: less than 48 hours from a late March 8th announcement of its plans to raise capital and a morning shuttering on March 10th.

As controversial as it was, Treasury and Fed officials fretted over the potential of massive bank runs when markets opened on Monday. It’s difficult to estimate the carnage we might have seen on Monday morning, but the plan to ring-fence the banks with deposit guarantees and a new lending facility from the Federal Reserve helped contain the crisis and prevent contagion.

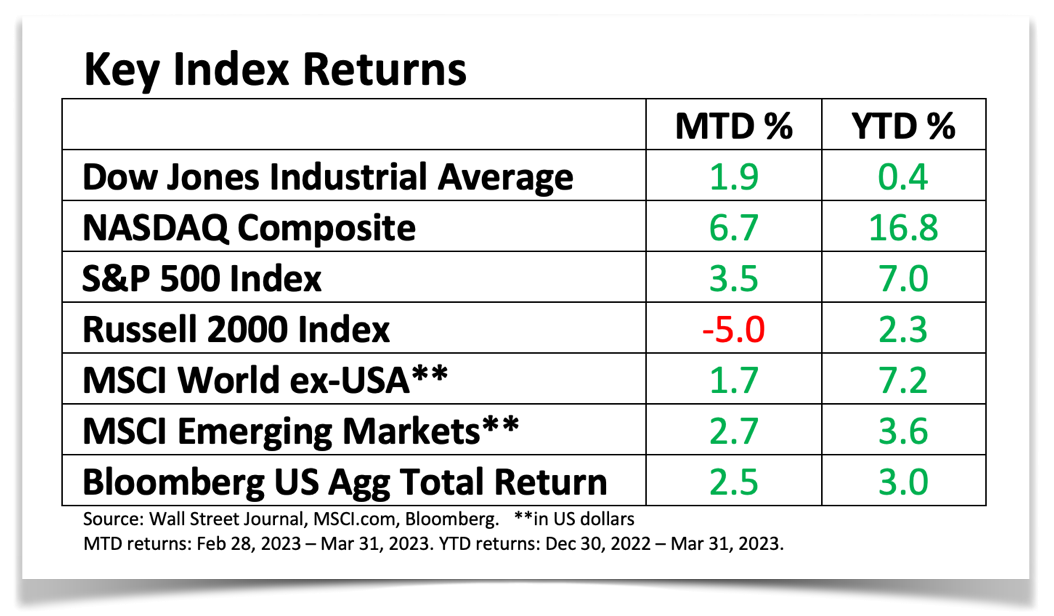

As the month came to a close, worries began to subside, and it was reflected in most of the major market indexes.

The Fed broke something

Regulators will dive into the details for a more thorough understanding of what happened, but the finger-pointing has already begun. Nonetheless, the impact may be felt for quite some time.

The Fed was probably on track to boost the fed funds rate by 50 basis points (bp, 1 bp =0.01%) to 5.00%- 5.25% at its March meeting. Inflation remains stubbornly high, but the Fed wisely chose to defer to banking stability, and opted for a cosmetic hike of 25 bp. It gives the appearance that inflation remains a priority, while focusing on the banking system. It also puts the Fed in a difficult position, as it hopes to tackle two conflicting goals: fighting inflation with rate hikes, which would put added stress on banks, or concentrating on financial stability.

The crisis might do the Fed’s job for it, as tighter lending standards slow economic growth. How much? No one knows. Inflation hasn’t been squashed, but problems with SVB have not spread to other banks. The crisis eased as the month came to a close, and most of the assets of the failed banks were purchased.

In recent days, sentiment has shifted on rates, but sentiment is ever-shifting. How the Fed reacts this year will depend on economic performance. As the months came to a close, fears have waned, helping shares rally, and the month ended on a favorable note.

What This means for Your portfolio

Unfortunately, there is still quite a bit of macro uncertainty. Will the Fed raise rates again? Are we headed into a recession? Are there potential rate cuts in the near future? Will the consumer continue to remain strong in this environment?

Unfortunately, there is still quite a bit of macro uncertainty. Will the Fed raise rates again? Are we headed into a recession? Are there potential rate cuts in the near future? Will the consumer continue to remain strong in this environment?

Ask two different financial experts these questions and you will most likely get two completely different answers. One area where there is some certainty – bond yields are much higher than they have been for 10 plus years. The current yields of 4% plus for short to medium term duration is quite meaningful.

As a result, for our upcoming 2023Q2 portfolio rebalance we are shifting some of the portfolio allocations into more medium term bond allocations. This provides a steady return while the market figures out which direction it wants to go. We think rate hikes are close to an end with a likely pause after that. In the next quarter or two the market should have a better sense of the depth of any upcoming recession and any equity repricing that my be needed. Until then, a well diversified portfolio and patience are the key to weathering any uncertainty.

We trust you’ve found this review to be educational and insightful. While we caution against making changes simply based on market action, ask yourself if your tolerance for risk changed considering this year’s volatility. If so, or if you have any questions or would like to discuss any matters, please feel free to give us a call. We are always here to assist you, answer your questions, and tailor any advice to your needs. Additionally, feel free to reach out to your tax advisor with any tax-related questions.

As always, we thank you for the trust, confidence, and the opportunity to serve as your financial advisors.

This research report has been prepared by the Centerline Wealth Advisors Investment Committee 2023©